It’s time for Place Advisory’s annual resale report, giving an insight into the performance of both new and resold apartments in the Inner Brisbane region.

Separating apartments into new and resold categories allows Place Advisory to breakdown the apartment market and provide better insights into what is actually happening.

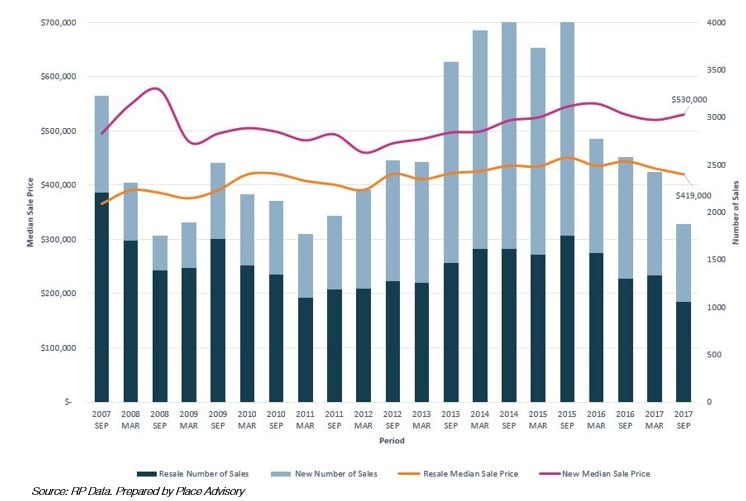

Inner Brisbane: New vs. Resold Apartments

*Please note that off the plan sales are recorded at settlement date and therefore, future reports may show more sales in recent periods than depicted in the graph above.

** Please note that for the purposes of this report, only the following suburbs are considered as part of Inner Brisbane: Albion, Auchenflower, Balmoral, Bowen hills, Brisbane City, Bulimba, Coorparoo, Dutton Park, East Brisbane, Fairfield, Fortitude Valley, Greenslopes, Hamilton, Hawthorne, Herston, Highgate Hill, Indooroopilly, Kangaroo Point, Kelvin Grove, Milton, New Farm, Newmarket, Newstead, Norman Park, Paddington, Red Hill, South Brisbane, Spring Hill, St Lucia, Taringa, Toowong, West End, Wilston, Windsor and Woolloongabba.

The above graph shows the number of sales of new and resold apartments and their median prices in Inner Brisbane over the past 10 years per six month period.

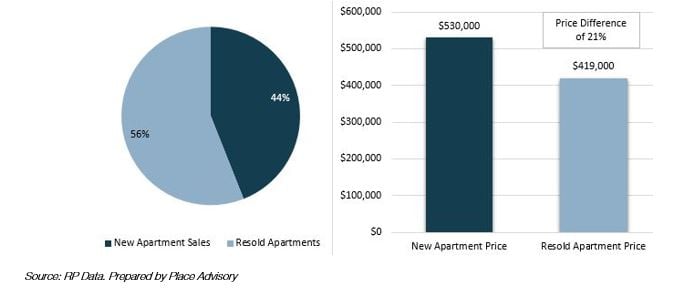

As can be seen from the graph above, apartments of both categories have had only minimal growth in prices of the last 10 years. Currently, the median price of a new apartment in Inner Brisbane is $530,000, while the median price of a resold apartment is $419,000. This represents a 21% price difference between new and resold apartments, above the 10 year average of 19%.

Inner Brisbane Apartments: Six Months to September 2017

Overall, sales volumes for apartments have been steadily decreasing since volumes peaked between 2013 and 2015. As sales volumes return to more normal levels the decline, not unexpectedly, appears more pronounced in new apartments. In the most recent period ending September 2017, 826 new apartments and 1053 second hand apartments were sold. Based on this, resales accounted for 56% of all apartment sales for the period, while new apartments accounted for 44%. The 1,879 total sales for the period is well below the 10 year average of 2661 apartment sales per six month period in Inner Brisbane.

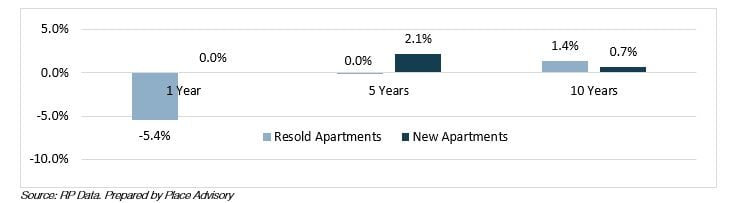

Annual Growth Rates: New vs. Resold Apartments

Annual growth rates have varied between new and resold apartments throughout Inner Brisbane over previous years. The graph above shows that over the last 12 months, resold apartments have been the most affected by market conditions, declining in price by 5.4% while, new apartments have remained steady. New apartment’s outperformed resold apartments over the last five years as well, recording growth of 2.1% per annum, compared to no growth for resold apartments. However, over the past 10 years resold apartments have increased by 1.4% per annum, compared to 0.7% per annum for new apartments.

Interactive Map: Inner Brisbane 12 Months to September 2017

Source: RP Data. Prepared by Place Advisory

*** Please note: Median prices and other information in the interactive map are based on 12 months of sales data ending September 2017. Areas are grouped by SA2 boundaries.

The above interactive map shows all the Inner Brisbane suburbs with a colour scheme based on the overall median apartment price in the area. Darker colours represent higher median prices while lighter, greyer colours represent lower median prices.

If you click around, you can see overall, new and resold median apartment prices, the price differences and average annual capital growth from resales for each area summarised for you.

The above interactive map clearly shows that apartments overall are more expensive in the areas east of the CBD on both the northern and southern sides of the Brisbane River. While apartments are generally cheaper on the western side of the CBD, the cheapest areas for apartments are found to the north in Newmarket, Wilston, Kelvin Grove, Herston and Red Hill, and to the south in Coorparoo and East Brisbane. It is no surprise that the cheapest areas for apartments generally tend to be furthest from both the CBD and Brisbane River. The average difference in price between new and resold apartments among Inner Brisbane areas is $125,194 while, the largest difference in price between new and resold apartments, $399,500, is found within the Brisbane CBD. The following table displays the biggest price differences between new and resold apartments for suburbs in Inner Brisbane.

Source: RPdata. Prepared by Place Advisory

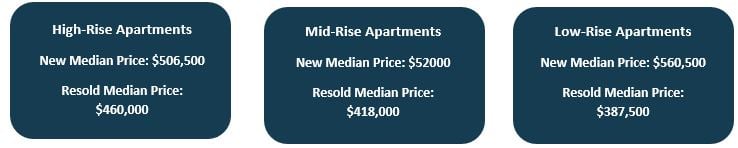

How Does Building Size Affect New and Resold Apartment Prices?

Following on from our last blog where we looked at how building size affected apartment performance, this time Place Advisory is taking a look at the impact of building size on the median price of new and resold apartments.

At the end of the September 2017 six month period, the most expensive new apartments were in low rise buildings, with a median price of $560,000. Mid-rise apartments were next with a median price of $520,000 while, high rise apartments had a median price of $506,500.

However, the reverse scenario exists with resold apartments where high-rise apartments are the most expensive with a median price of $460,000, followed by mid-rise apartments which have a median price of $418,000 and low-rise apartments with a median price of $387,500.

The largest differences in price between new and resold apartments are found in low-rise buildings where the price difference is 44.5%. This decreases to 24.4% for mid-rise apartments, and there is only a 10% difference for high-rise apartments.

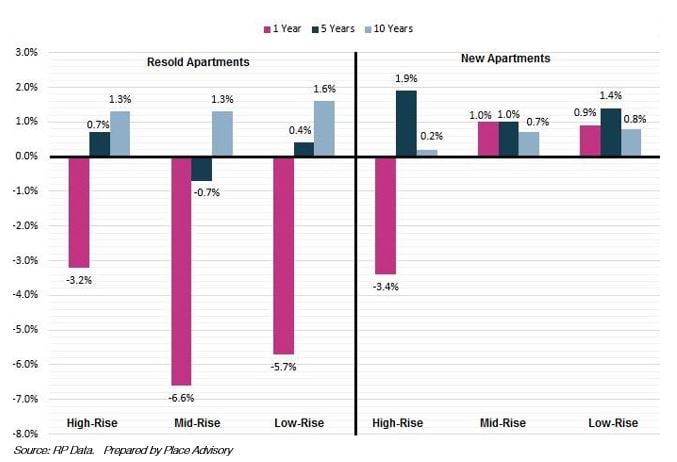

Annual Growth Rates by Building Size: New vs. Resold Apartments

When we look at growth rates over one, five and ten years we see that resold apartments have generally been falling in price the most over the past year. The biggest fall in median price over the past year to September 2017 was in resold mid-rise apartments which fell by 6.6%. Only new mid-rise and low-rise apartments recorded positive growth over the past 12 months to September 2017. When considering the last five years, new high-rise apartments recorded the most growth of 1.9% per annum, whilst resold mid-rise apartments recorded the least at -0.7% per annum. Over the previous 10 years, resold low-rise apartments recorded the most growth at 1.6% per annum whilst, new high-rise apartments recorded the least at 0.2% per annum.

Highlights of Inner Brisbane Apartment Market: 12 Months to September 2017

Most Expensive New Apartments: Brisbane City - $850,000

Most Expensive Resold Apartments: Newstead - $675,500

Resold Apartments Best Average Annual Capital Gain: Paddington – 8.1%

Longest Average Holding Period: Wilston – 16 Years

Summary

While the media may continue to report a struggling apartment market in Brisbane, not all apartments are under performing. Construction levels of new apartments are steadily reducing while, affordability remains at reasonable levels, especially when compared to Sydney and Melbourne. Current conditions offer a great entry point into the market which has plenty of potential for future growth.