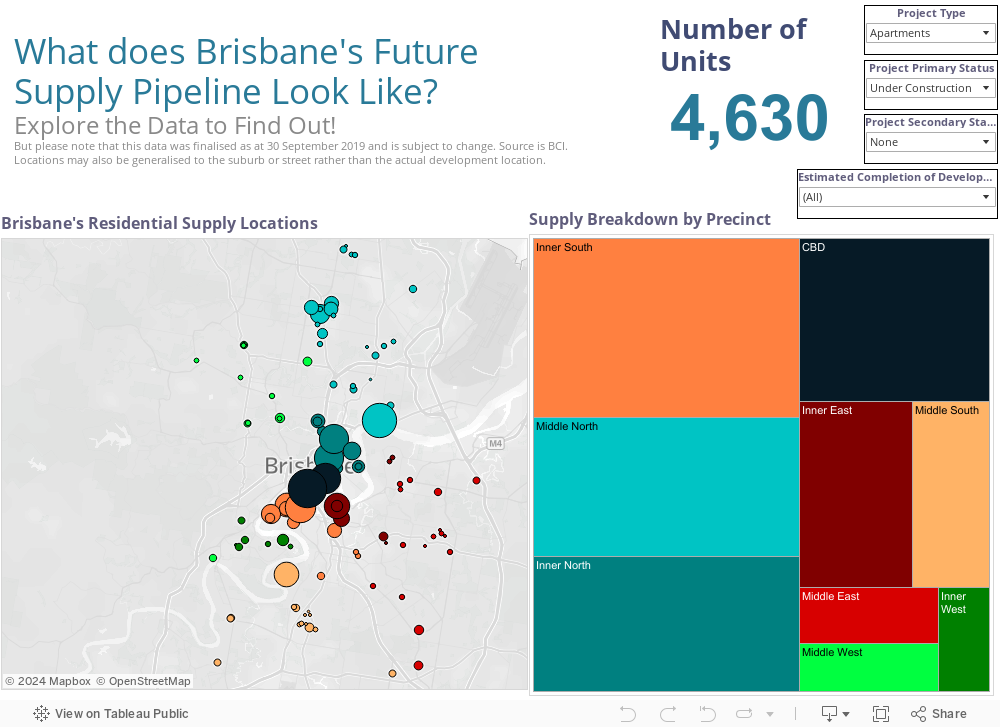

In this quick property blog Place Advisory takes a look at the future Brisbane Unit Pipeline. With Brisbane having passed the peak of the cycle, the outlook for the next few years is changing. We have tracked all development applications from the online BCI database and summarised what the market will look like in terms of completions, pending developments, deferred developments and location of supply. In the following interactive dashboard that we have designed, you can use various filters to explore the supply pipeline and see how it compares in different periods.

Use the filters in the top right corner to narrow down your search. The map on the left shows the location of developments while the tree map on the right shows the share of total selected supply by precinct. Colours represent different precincts of Brisbane. Click on a precinct or development to highlight it on both graphs.

Prepared by Place Advisory. Source: SQM Research.

Developments have been included where the expected completion six month period is from the second half of 2019 onwards or unknown. Data was collated as at 30 September 2019. Please keep in mind that there may be minor differences to the actual market due to database status updates. The six-month period in the year 1900 indicates that there is no stipulated expected completion date.

By exploring the development pipeline, the extent that Brisbane has passed the peak of the construction cycle is clear. The second half of 2019, of which we have already progressed through the majority, sees approximately 1500 apartments complete construction in both inner and middle Brisbane compared to just over 2000 in all of 2020. Beyond this there is minimal apartments that are currently under construction that are expected to complete.

While there are more apartments approved or in the application stage, many of these are likely to be pushed back as it remains difficult for developments to come to market. As such there is a portion of the supply pipeline that will never come to market. This is further emphasised by the large proportion that is currently abandoned, deferred or has the site up for sale.

The CBD, Inner North and Inner South, remain the precincts with the biggest share of unit supply. Brisbane’s inner and middle west precincts currently have only very low levels of supply under construction and are likely to see demand far outweigh future supply as the market continues to evolve.